A Lot to Think About

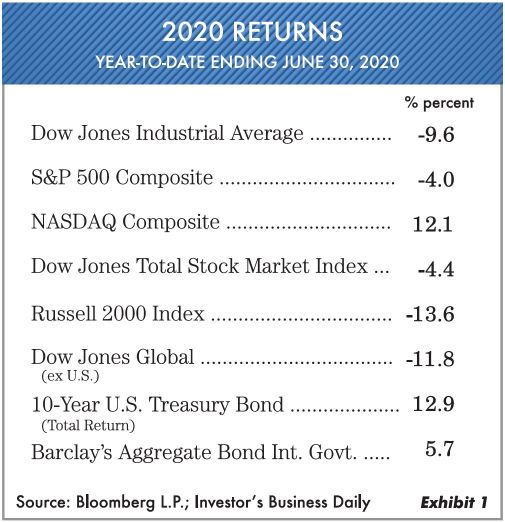

No one would have predicted or expected the first six months of 2020 to end like they did. Confusing and scary are two words that come to mind. This year so far seems like three years in time as we have had to deal with so many unexpected things. There still seems to be a cloud of depression and lack of good expectations among most investors. In this issue we hope to address the reasons for volatility and what the Federal Reserve has done to the investing landscape. As topsy-turvy as the past six months were, we show the returns for the period ending June 30, 2020, as measured by various major market measurements in Exhibit 1.

Why Did the Market Go Up with All the Bad News After March …?

The number one question we have received over the last three months is “Why is the market up?” Looking back, as 2019 came to an end we felt like it was 1999 once again (see our January 2020 Market Comments). Everything seemed expensive and crazy in the stock market at that time. Sure enough, it played out that way with the COVID-19 virus being the tipping point.

As the markets were falling apart in late February and into March, we weren’t surprised to see the Federal Reserve lower interest rates basically to the zero level. Under historically normal circumstances the market, after a sharp decline, would rally short term and then fall again as sellers come in. What we didn’t see and don’t think anyone else saw was the incredible amount of money the Federal Reserve threw into the economy. Exhibit 2 shows 10 different ways the Fed (with the U.S. Treasury’s OK) put cash into the economy. Such extensive moves have never been made before.

These collectively are the reasons the markets went up. (When the government decides to own virtually everything, it has the power to push up financial asset prices.) Unfortunately, all those people who don’t own stocks and bonds cannot participate. The wealth disparity continues to accelerate in the U.S., and the Fed is primarily responsible. Now we have every small investor and person on the street using their government money to buy stocks. Why not? No commissions and no one is working, so let’s gamble awhile. In our investing career we have never seen a more irresponsible Federal Reserve. That’s why stocks moved up starting in late March. At Oxbow we thought it would be a short fake rally, but that was before the Fed decided to throw everything at it. However, their moves just postponed the eventual pain of extremely overpriced assets, which is occurring. That’s the primary reason we at Oxbow have more liquidity than normal.

How Much Risk Should an Investor Take …?

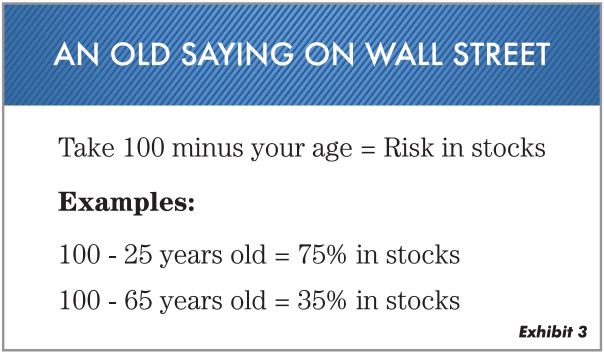

In many ways, in our opinion, most investors are taking too much risk in today’s markets. There are numerous reasons, but the primary reason is “recency bias,” i.e., whatever the most recent experience has been has a profound effect on investor thinking. Since we have had 11 years of markets moving up and interest rates moving down, investors have become complacent. In addition, every time the stock market has fallen the Federal Reserve has been there to rescue it in one form or another. Sad to say … the Fed has completely forgotten about what their true mandate should be, but it still exists. Here in Exhibit 3 is an interesting flashback:

While this simple formula for measuring risk has been around for many decades, it still has some credence today. Perhaps, in today’s investment atmosphere, we should adjust it to “90 minus your age.” Most investors are probably carrying too much risk today—for the reasons previously mentioned. In Oxbow’s new book (to be published in December 2020) titled Your Money Mentality, we discuss many factors regarding a person’s risk. Part of how much risk investors take depends on what mood they’re in. If they have just had a great year or a windfall, they’re more prone to risk. If they’ve had a financial setback or were diagnosed with a fatal disease, they’re inclined to be more conservative.

Every financial group wants you to complete a risk-tolerance questionnaire. First of all, they assume you know how much risk you’re comfortable with, but really if you knew that then why take the quiz? In our experience at Oxbow, the similarity of investors’ risk tolerance is all over the map. Some investors say they’re aggressive but want CDs, while others say they’re conservative but want all stocks. At Oxbow we try very hard to find out what an investor can live with in terms of volatility and temporary loss of capital. In addition, we ask a host of other questions about personalities in relation to investing. As an example: “Do you ever spend a day without looking at the stock market?” We still believe that risks are higher than normal if you consider some of the macro themes in Exhibit 4.

So Where to Invest …?

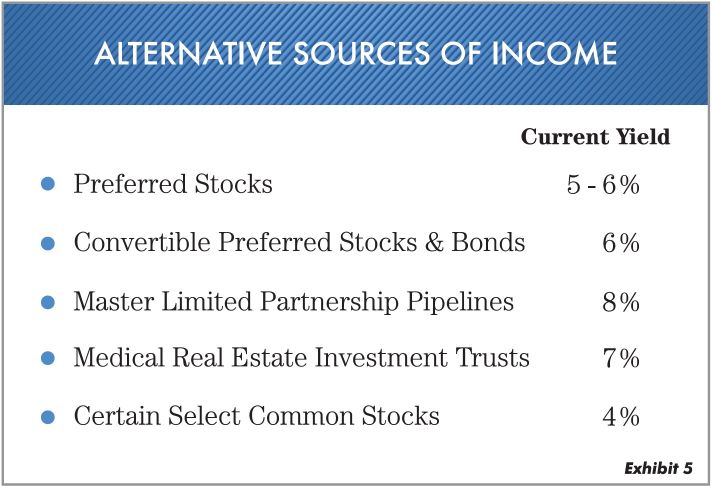

There are pockets of areas to invest in currently, but everything you do needs to be measured. The current interest rate on a 30-year U.S. Treasury is 1.4%, and the one-year CD rate is 0.25%. So, you can see there is basically no return here. In addition, stocks are expensive. The stocks we at Oxbow own have low debt and visible earnings and dividends. They likely can withstand tougher times. We have a number of income items also that create a better return. Notice income items in Exhibit 5.